New research released Monday by the Corporation for Enterprise Development, a nonprofit, illustrates key facts about financial insecurity and inequality in the U.S. -- and shows how these features of our economy put women and people of color at a major disadvantage.

The household wealth gap between whites, Asians, Latinos and black Americans is particularly staggering, with the median household net worth for white families now standing at 15 times that of black households.

People of different groups have wildly varying degrees of access to employment, education, home ownership and savings, which also contributes to the massive economic divide.

According to the CFED study, the economic status quo has made it "next to impossible" for many Americans to climb out of poverty, as systemic disadvantages create a crushing financial spiral that often leaves people unable to save modestly for unforeseen expenses -- let alone put away more robust savings to build equity.

“Making ends meet for these families requires constantly juggling a series of complex choices and often ‘robbing Peter to pay Paul’ just to manage week-to-week finances,” CFED President Andrea Levere said in a statement.

When someone is struggling, financially or otherwise, we often encourage them to "pull themselves up by their bootstraps." But what's largely forgotten today is that this expression originally meant "to try to do something that's impossible." The key findings from CFED's 2016 report show that it's more ridiculous than ever to expect disadvantaged Americans to pull themselves up by their bootstraps -- because in many cases, the economy seems to have taken the shoes right off their feet.

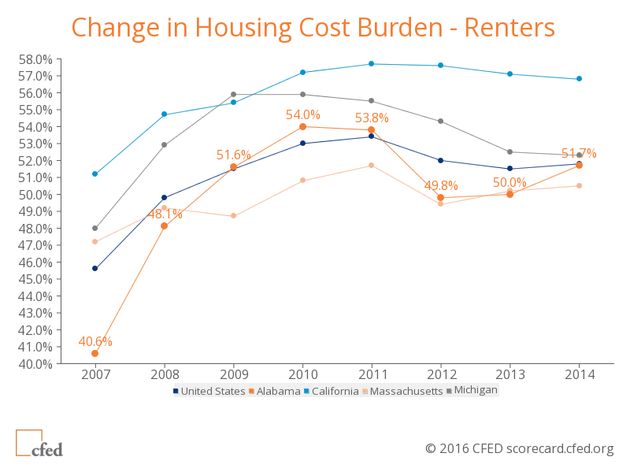

1. Fewer homeowners + more renters = Less savings.

Since the Great Recession, home ownership has fallen to its lowest levels since 1967. Consequently, more Americans are renting, and more than half of them are seeing a big chunk of their income gobbled up in housing costs, thanks in part to a lack of affordable housing nationwide. With money going to the property owners, renters have no opportunity to build equity on homes themselves.

Furthermore, CFED reports that a whopping 51.8 percent of all renters are “cost-burdened," meaning they spend over a third of their income on housing.

With less money available to spend on food, health care, child care and other expenses, financially troubled consumers commonly turn to short-term loans.

Which brings us to the next problem...

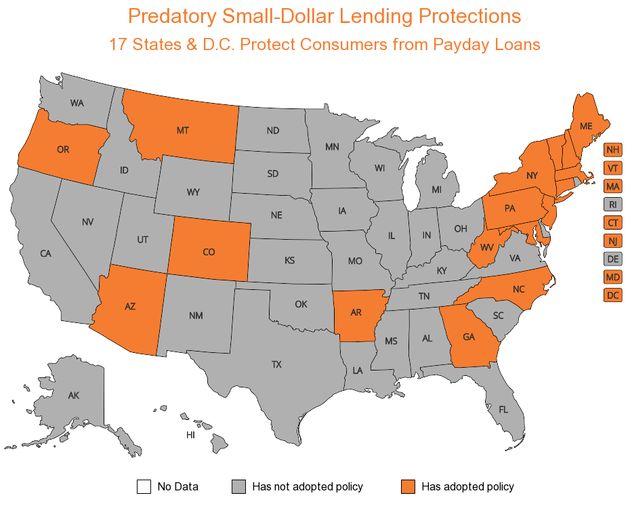

2. Predatory lenders are still being allowed to prey.

Alternative financing schemes like payday, auto-title and short-term installment loans are often the only way that Americans with low or no credit histories can make it to the next paycheck.

CFED reports that more than 1 in 10 households with incomes below $30,000 have used alternative financing schemes, whose sky-high interest rates and short payback periods can push borrowers into a cycle of unrelenting debt.

Regulation of such loans, whose annual interest rates can be as high as 400 percent, is weak and uneven. Just five states -- Connecticut, New Jersey, New York, North Carolina and Pennsylvania -- have prohibited or capped such predatory loans, CFED reports. A total of 17 states regulate predatory lending practices, either by barring payday loans entirely or by capping interest rates at 36 percent.

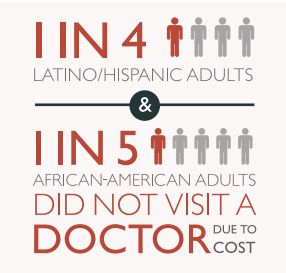

3. Health care has become a luxury.

For people who already struggle to pay for housing, food and child care, health care expenses tend to get put on the back burner. In a 2014 survey, 14.3 percent of adults nationwide said there'd been a time in the past year when "they needed to see a doctor but could not because of cost," according to the Kaiser Family Foundation. The rate was even higher among black and Latino adults.

The CFED report notes that the Affordable Care Act has helped bolster the number of insured Americans, especially within communities of color, and said the ACA "underscores the important role states can play in implementing federal policy."

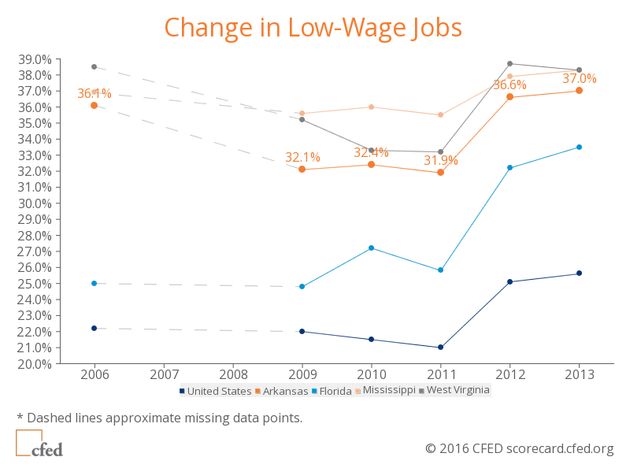

4. Even if you can find work, there's a good chance it won't pay well.

Mid-wage and higher-wage jobs were among the biggest casualties of the labor market downturn (as measured from January 2008 though February 2010) following the Great Recession, according to the National Employment Law Project. During the recovery period over the next four years, it was low-wage jobs that surged.

CFED reports that jobs paying an annual wage below the national poverty line account for more than a quarter of all jobs. In nine states, nearly all of which are poor and in the South, more than a third of all available jobs are low-wage. Six of those nine states, CFED notes, have comparatively high populations of black and Latino citizens.

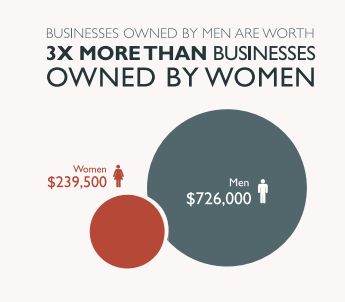

5. Minority- and women-owned businesses face a massive valuation gap.

When unemployment spiked during the economic downturn, it prompted many out-of-work Americans to turn to self-employment, CFED reports. The gap between white and black business owners, in particular, narrowed. But the gap between the net worth of business owned by white people and the net worth of businesses owned by black people did not.

The average white-owned business has a net worth nearly triple that of the average minority-owned business -- $656,364 compared to $224,530 -- and the gap is no better when it comes to gender.

Businesses owned by men are on average worth over three times more than businesses owned by women -- the difference is $726,000 versus $239,500.

Original Article

Source: huffingtonpost.com/

Author: Kim Bellware

No comments:

Post a Comment